A payment method that is becoming increasingly prominent – and which could help B2B platforms offer a real point of differentiation to their competitors – is open banking. Open banking payments are direct account-to-account (A2A) transactions, with money moved along a single set of rails with no other third parties involved, making them cheaper, faster, and more secure than card or wallet payments.

How your B2B platform can benefit

Imagine that alongside your embedded payments offering, which gives your merchants the possibility to support card, wallet and other payment methods, you can also provide your merchants with a payment method that is cheaper, faster, and more secure than cards or wallets.

With this you benefit from a powerful new feature that opens up a new revenue stream, while simultaneously making your platform stickier for your customers. And your merchants benefit in a number of ways also, particularly from a) cheaper (up to 90%!) transaction costs – giving them greater pricing power, b) almost zero fraud, since customers need to authenticate the payment in their bank app, rather than with card numbers, and c) instant settlement – meaning faster cashflow when compared to cards, which take 1-3 days to settle.

The challenge: Every open banking provider has its limits

Open banking payments are growing fast. By the end of 2021 in the UK, almost 27 million open banking payments had cumulatively been made, which was an increase of more than 500% in twelve months, while research suggests that global open banking payments volume will exceed $116 billion in 2026, from just under $4 billion in 2021. Offering open banking payments to merchants on your platform right now puts you ahead of your competitors, reinforcing your reputation for innovation, and making it less likely for them to leave you.

Furthermore, there are a growing number of open banking providers on the market today, and many of them are investing heavily in product development. But there is a catch.

Building an open banking provider is highly complex. On the technical side, different markets have different API standards, banks have their own individual specifications and requirements, and maintaining all these connections is a headache. On the licensing side, different licenses are required in the UK and EU. And where Payment Service Providers have been building out infrastructure to support digital card payments for 15-20 years in some cases, open banking was only really kick-started in 2018 under the PSD2 regulations, meaning the market is much less mature.

For these reasons, every open banking provider on the market today has limitations in terms of market coverage, in spite of heavy investment in product. As a B2B platform company, your merchants have diverse needs, including a range of bank connections and geographical reach. There is no single open banking provider on the market today which will meet these requirements.

Introducing multi-rail open banking

However, there is an option to embed open banking payments into your product offering – multi-rail open banking.

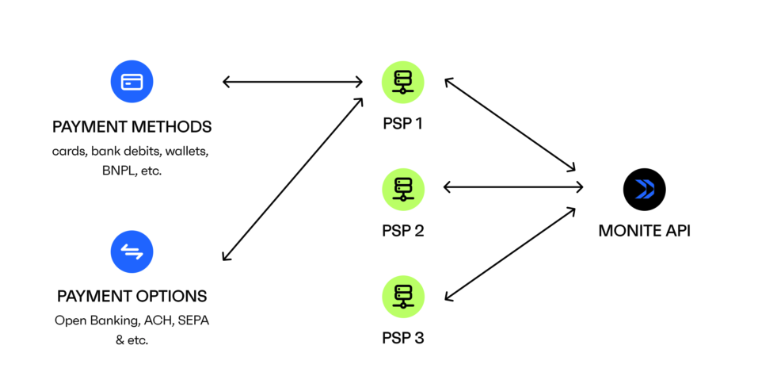

As you can see, a multi-rail open banking solution aggregates a range of open banking APIs and brings all these together under a single Monite API.

With a multi-rail approach, you benefit from the strengths of multiple open banking providers. So no matter what limitations an individual open banking provider may have in terms of number or quality of bank connections, licenses or so on, you will be able to ensure that merchants on your platform can benefit from low cost, low fraud, and fast payments.

The big opportunity: building to be best in class, buying to be all-in-one

And beyond these benefits, there is a much bigger long-term prize. Resources dictate that most B2B platforms need to make a choice whether to build a best-in-class solution, or an all-in-one solution. But actually, there is a third way, which combines the best of both worlds.

Embedded finance specialists such as Monite build financial automations at scale, and multi-rail open banking is only one of the products that are available.

Consider the huge range of financial automations that your platform could offer – invoicing, payroll, accounts payable, and expense management, to name a few. Building these out internally is a daunting task – expensive, time-consuming, and incurring huge technical debt.

In comparison, by partnering with a provider such as Monite – which has already solved complexity and edge cases at scale – you can retain a core focus on building what makes you best in class, while simultaneously buying products that make you an all-in-one solution for your B2B customers. With this approach, you are in a position to leapfrog competition on either side of you, both those competitors building for best in class, and those building for all-in-one.

All the while ensuring your solution is extremely sticky and with multiple ways to monetize.